Ending not with a bang, but a whimper [Q4 2022 Portfolio Update]

Ending not with a bang, but a whimper [Q4 2022 Portfolio Update]

The content of this post, or any post on Stumbling About, is for informational purposes only and does not represent investment advice. You should do your own research before using any of the information that we share, and especially before investing.

Bubbles extending

Investing right now is a fascinating experience. Put “this time is different” aside for a second because that saying is played out. However, the multitude of factors we’re working with in the US economy, the global economy, and geopolitical affairs is on a whole new level.

Inflation seems to be cooling, but I bet it’s gonna be around for longer than the market is pricing in. Which means that we’re gonna see reasonable interest rates (4%+) also for longer than the market is pricing in (see my post here for my view on near term interest rates). Coming off a record-inducing bull run, this has created a massive bubble situation. And yet…my bubble indicator isn’t saying we’re done yet, which is why I’m staying “bullishly pessimistic”.

I think that 2022 was a mini relief valve for the market kicking out a 20% decline just because we couldn’t take anymore. Predictions are worth making, but the position that I’m taking is positioning myself for another rally that will be close to the prior peak (at least) before we see a tumultuous market decline. I desperately hope that this market fall doesn’t happen, but there are too many factors that are priming the pump — the biggest of which, in my opinion, is that consumers of all types are setting themselves up for financial failure (not enough long term cash, too much debt, not respecting jobs, etc.).

On that happy note, here’s my portfolio summary from 2022! 😎

The usual context setting

My portfolio is primarily based on a Long Trend Momentum model that I created called Farfin. You can learn more about Farfin here. In addition, I will usually also have a relatively small investment in broad market ETFs, concentrated mostly in the Vanguard Total Stock Market Index ETF (VTI)1.

The combination of these typically results in my investments based on Farfin being 90%+ of my portfolio. However, I will opportunistically pick up other stocks when the market calls for it. As of the end of Q4 2022, my portfolio was roughly an 85%/15% split between Farfin and non-Farfin, respectively.

Most of this post will look at the combined portfolio, but I do highlight Farfin performance specifically in the “High level quarter summary” section.

High level quarter summary

Results2: The overall portfolio was up +18.2% for the quarter and down -18.5% for the year (shucks) — you ever get that feeling that you hit the shot right at the buzzer….and then still lost? Yeah, that’s my portfolio this year…

Market Results: As a reference point, the market (VTI) was up +7.1% for the quarter and down -19.5% for the year — I know you all expect (and deserve!) better. Shame, shame, shame. 🥺

Buys: Back to (mostly) boring, no new pickups this quarter….though I did get up to some Alibaba call options shenanigans, which you can read about later, and put more into Twilio and Meta.

Sells: Once again, please see Alibaba shenanigans…otherwise, nothing sold.

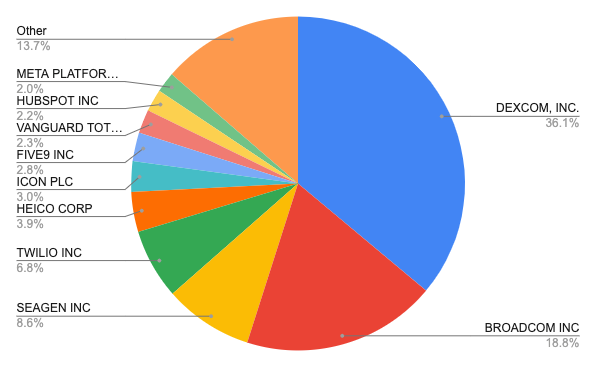

Top Holdings: DexCom remained my #1 holding at roughly 36%, and here’s the full top 5:

DexCom (DXCM): 36.1%

Broadcom (AVGO): 18.8%

SeaGen (SGEN): 8.6%

Twilio (TWLO): 6.8%

HEICO Corp (HEI): 3.9%

Top 10 holdings cumulatively: 86.4%

Below is a pie chart of my top 10 holdings for those that enjoy visuals.

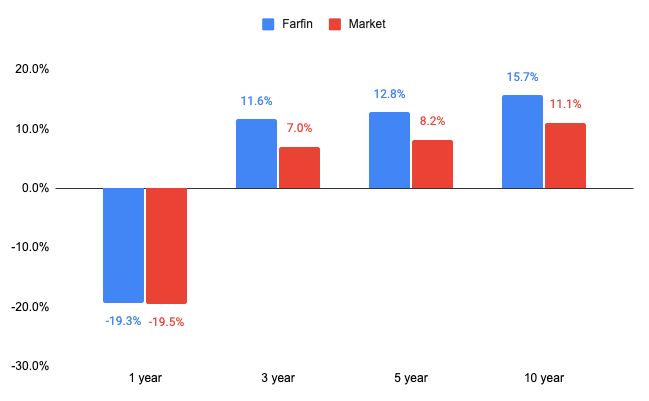

Farfin-specific summary

Since it’s the end of the year, I’m going to take a little space to give a summary of Farfin’s performance specifically (reminder that Farfin is the model that dictates the bulk of my portfolio investments).

Below is a quick look at Farfin’s 1 year, 3 year, 5 year and 10 year performance (CAGR3) vs. the market.

I expect Farfin to outperform the market roughly 60-70% of the time, and this year they roughly matched. Below is the year-by-year breakdown of Farfin v Market over the last decade.

Lowlights and Highlights

Lowlights

As I said last quarter, the biggest lowlight for the quarter is a macro one — this was a sucky year.

As far as specific stocks go, Trupanion (TRUP) lost all interest in generating positive returns, losing about -20% for the quarter and over -60% loss for the year. 😤

Twilio (TWLO) was a newcomer last quarter, and due to some continued drops during this one, I kept buying, building Twilio up to almost 7% of the overall portfolio. Don’t let me down, Twilio!

Here are the 5 bottom feeders for the quarter (full year returns in parentheses):

Trupanion (TRUP): -20.0% (-64.0%)

Twilio (TWLO): -11.5% (-14.3%)

LendingTreet (TREE): -10.6% (-82.6%)

Five9 (FIVN): -9.5% (-50.6%)

SeaGen (SGEN): -6.1% (-16.9%)

Highlights

Through all the torment, there are actually highlights from the quarter. Nothing to write home about, but worth enough to blog about 😊

Here’s the full top 5 quarterly best performer list (full year returns in parentheses):

Alibaba Call Options (BABA 01/20/2023 80.00 C): +302.4% (+302.4%)

Dexcom (DXCM): +40.6% (-15.7%)

Broadcom (AVGO): +27.0% (-13.4%)

TransDigm Group (TDG): +20.0% (+1.9%)

Makita Corp (MKTAY): +19.8% (+20.0%)

I’ll get to Alibaba in a second. Before that, obviously Dexcom and Broadcom are huge wins for the quarter given that collectively they represent ~55% of the overall portfolio. I think they may have forgotten why I own them, but after a quick pep talk they got back to work.

During the quarter two things happened with Dexcom: first they released some quite positive forward looking guidance during their Q3 earnings call, and second their latest product (the G7 continuous monitoring device) got FDA approval. The market (and by association, Doogles) quite enjoyed this double whammy.

Also, I was really happy to see TransDigm start to gain some steam. I love that stock, it crushed for me back in 2020, but took a couple year performance hiatus before jumping back on the saddle — hoping this continues!

Alibaba shenanigans

I bought Alibaba stock in Q4 of 2021 with the expectation that I’d hold the stock for 2+ years, planning to sell when it got to a fair-ish valuation over $200 per share. China and China/US relations continued to get into a whole heap of nonsense since then so $200/share became a near term pipe dream. I still feel like Chinese officials spent 2021 and 2022 sitting around in Hunger Games Capitol Residents attire spinning a wheel to determine which industry to take down next.

From when I bought to October 2022 Alibaba did not do…well.

Then, in late October, news from China hit Alibaba (and other Chinese stocks) quite hard — Alibaba dropped ~20% in one day on October 24th, falling to ~$60/share. What to do, what to do?

At this point, I gave myself three options of what to do with the stock:

Double down!

Sell and completely cut ties (getting a little tax write off from the loss)

Ride it out like a boss

I really didn’t like option #3, I didn’t have enough long term conviction in the stock for option #1, and option #2 made me sad.

Giving the situation more thought, I figured that Alibaba was so beaten down that dropping by more than another 20% sounded far fetched (that doesn’t mean it wouldn’t happen, but it seemed unlikely), and any good news would send it soaring. So I created a fourth option: sell the stock outright, and then buy options.

Options are not to be messed with, and I don’t recommend this for anyone, including myself. However, a stock where (according to my assessment) there was very limited short-term downside and sizable short-term upside sounded like the right play for options if there ever was one. And I saw a solid chance that good news was going to come from China over the following 3 months (sometime between November and January) in the form of one or all of the following:

President Xi easing Covid restrictions

Improved US/China relations

The US audit of Alibaba’s books going well

So I bought call options expiring on 1/20/2023 to account for the time frame of the potential news listed above. And running some calculations on the strike prices, decided to buy at an $80 strike price. As for the the amount to buy, I put roughly ~20% of the proceeds from the sale of Alibaba stock into this (remember that I thought that if the stock did drop it wouldn’t go down more than 20%…so I figured I’d be losing the same amount that I would if I held onto the stock if this trade went south). And voilà! Now I was a holder of Alibaba options.

I bought the options at a ~$2/contract premium and set a sell limit order at $26/contract (this was effectively a bet on Alibaba hitting $100/share from the ~$60 price point it was sitting at).

As the year came to a close I started to chicken out and changed my limit order to $13/contract. This triggered on January 4, selling out the options position for a 6x+ return overall. Not bad! However, after selling, Alibaba (almost immediately) began to shoot for the moon, hitting $120 per share on January 20. I’m still happy with my 6x return, but if I hadn’t chickened out, then my original limit order would’ve gotten me a 13x return, and holding out until the option expired would’ve led to a 15x return.

Alas, I really shouldn’t complain and it was quite a ride!

Looking to the future

Overall: This year was weird, and painful. I’ve said this a few times now, and I continue to believe that in the medium term, we have some more downward market reckoning to deal with, but I expect some material rallying before that takes place.

To sell: Nothing on the horizon to sell (aside from the BABA call options which I had to offload on or before January 20, 2023)

To buy: Most likely nothing, aside from the Farfin-based buys that I made at the start of the year. You’ll need to stay tuned for the Q1 2022 round up in 3 months to see what those are.

Oh, and if interested, you can see my whole end of Q4 portfolio here — these are all my holdings, along with performance for the quarter. Enjoy!

The content of this post, or any post on Stumbling About, is for informational purposes only and does not represent investment advice. You should do your own research before using any of the information that we share, and especially before investing.

Throughout this and other posts, when I refer to a stock’s performance relative to “the market”, I’m using the Vanguard Total Stock Market Index ETF (VTI) as the proxy for “the market.”

All of my returns are calculated using time-weighted returns. You may also notice that my Q3 2022 return is different than what I showed in my last post. I noticed a calculation error and corrected it for this post.

CAGR stands for the Compound Annual Growth Rate (i.e., the rate at which the portfolio/market changed each year). You can read more about CAGR here.