Things are getting INTERESTing

Things are getting INTERESTing

aka, when will interest rates stop going up

The content of this post, or any post on Stumbling About, is for informational purposes only and does not represent investment advice. You should do your own research before using any of the information that we share, and especially before investing.

What the Fed’s been up to

In case you haven’t heard, the Fed1 has been increasing interest rates at a pretty sizable clip in order to fight decades-high inflation. Let’s visualize that “clip” — here’s the Fed Funds Effective Rate2 since 2009:

It’s not so much that the current rate of 3.75% is high (in fact it’s not, historically speaking). Rather it’s that just 10 months ago the rate was 0%, and this kind of increase trajectory could send shockwaves through an economy (and it likely is about to!).

So, the golden question — when does the madness stop?!?

Spoiler alert: I don’t know.

But not knowing has never stopped me from speculating. So let’s get to the speculation!

Grounding context

First, some context to ground us:

The Fed targets an inflation rate under 2%

So far in 2022, the inflation rate has peaked at 8.2% in September

In recent months, inflation has shown some signs of reversing

Historically, high inflation has been defeated when the Fed Funds rate gets above inflation

The Fed has vowed to crush inflation at all costs

For the sake of this speculation, let’s take the Fed’s “all costs” notion at face value, and also assume that history holds and the Fed Funds rate has to get above inflation for it to come down.

Forecasting inflation

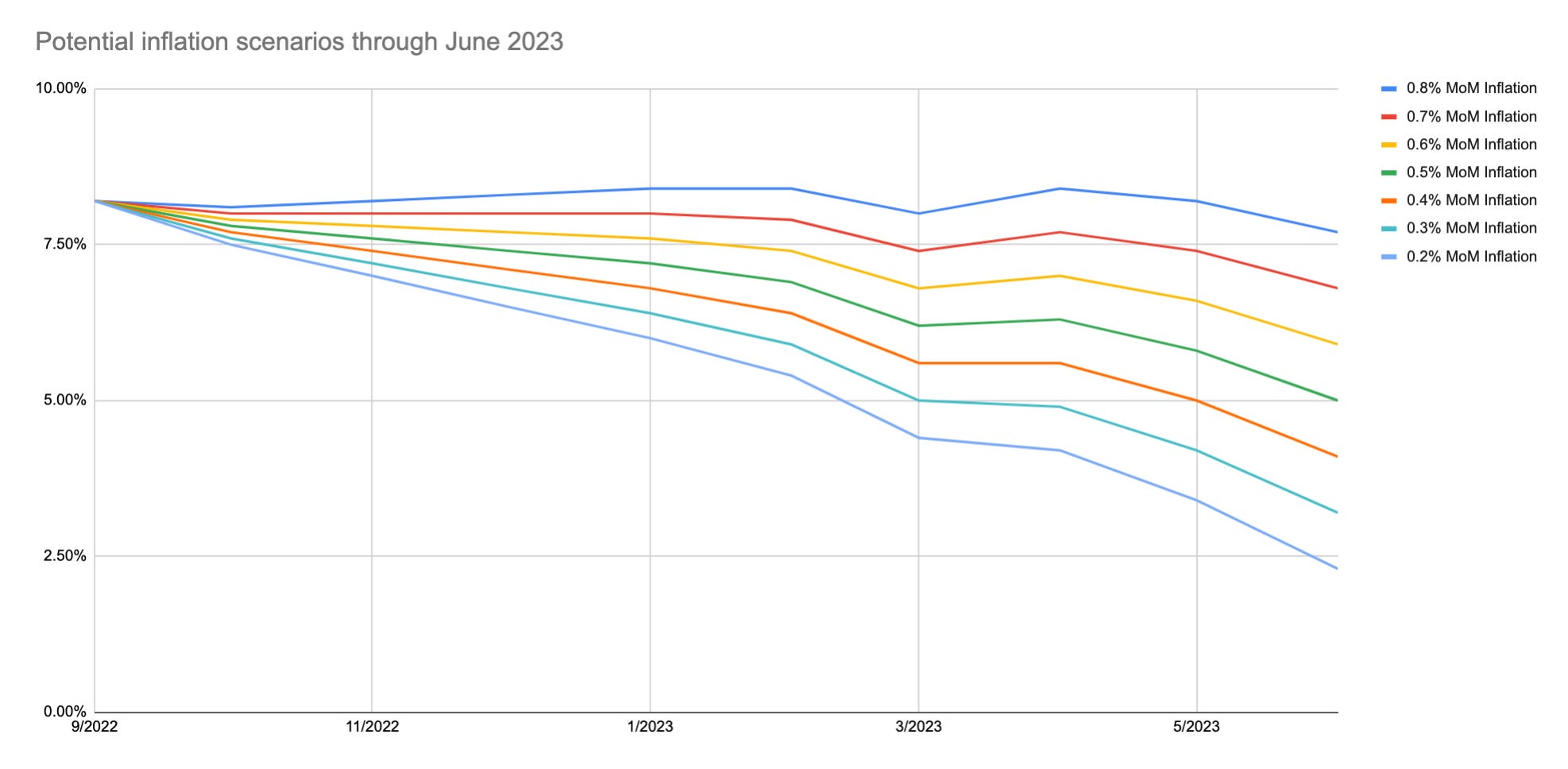

OK, now, let’s look at some recent month over month inflation changes3 to forecast out some potential scenarios on where inflation can go. I’m going to use a monthly average increase range from 0.2% to 0.8% (a pretty good range given recent changes) to lay out the scenarios:

In these fictitious scenarios, in June of 2023 inflation will land in a broad range between 2.5% (close-ish to where the Fed wants it) and 7.5% (far from where the Fed wants it). So you can see that, at a high level, the Fed wouldn’t just feel comfortable sitting back letting that high end of the range play out. There’s definitely still work to do.

Jerome Powell4 ^^

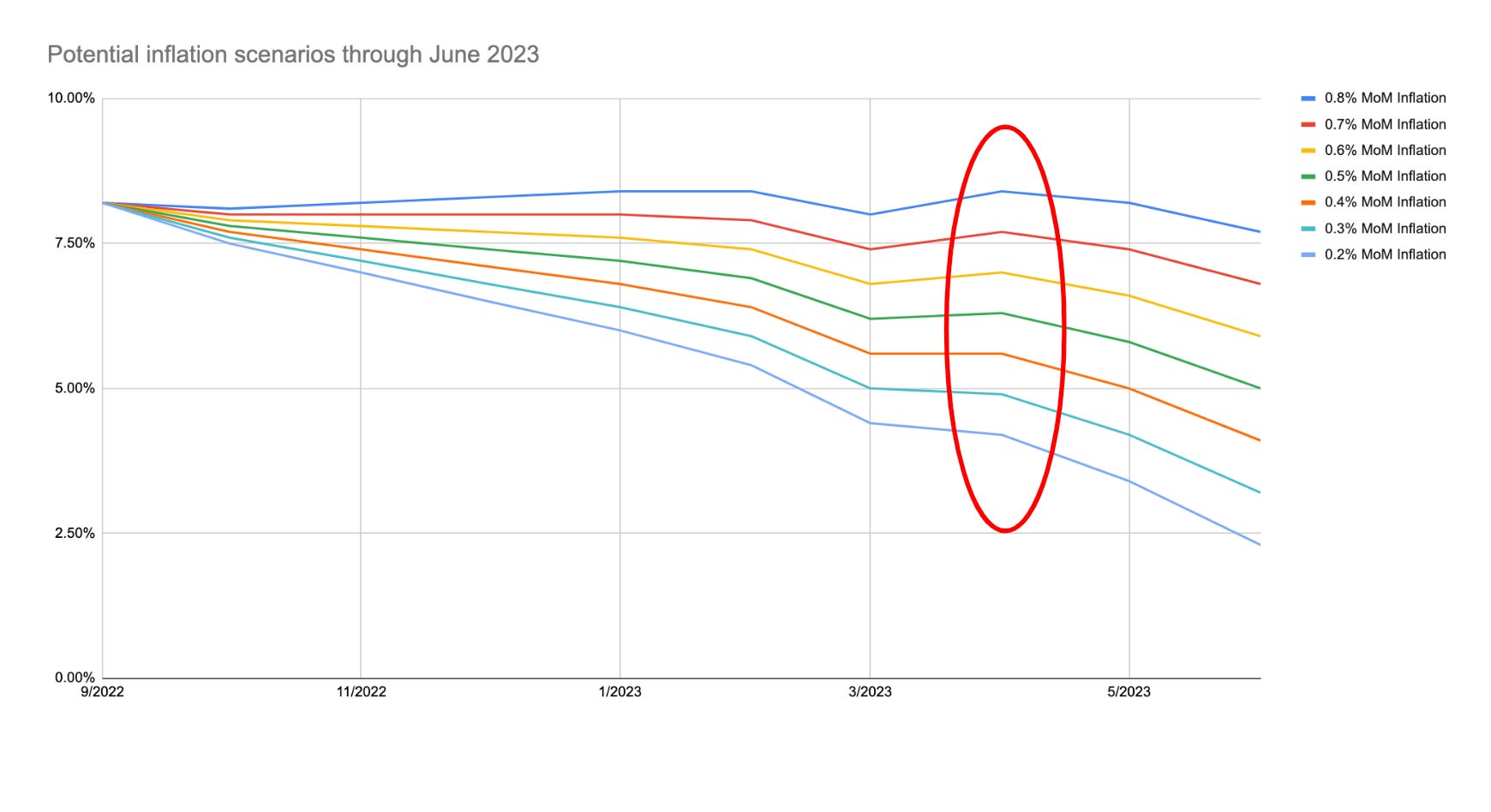

The place to pay particular attention to in this graph is not June 2023, but the peaks (because this is the inflection point the Fed would need to conquer) in April.

This range is a little higher at 4.2% to 8.4%. Given all the supply issues + consumer demand issues that we’re fighting against, an average of 0.2% month over month inflation is unlikely. And given recent trends, so is 0.8%.

So let’s tighten the range and say that the 0.4% to 0.6% month over month is a range to bet on5. This would mean that the near term inflation peak range is more like 5.6% to 7%. In this world that I just created, that is where the Fed would need to land!

Fed Funds rate scenarios

So how could the Fed get there? Let’s run through some scenarios.

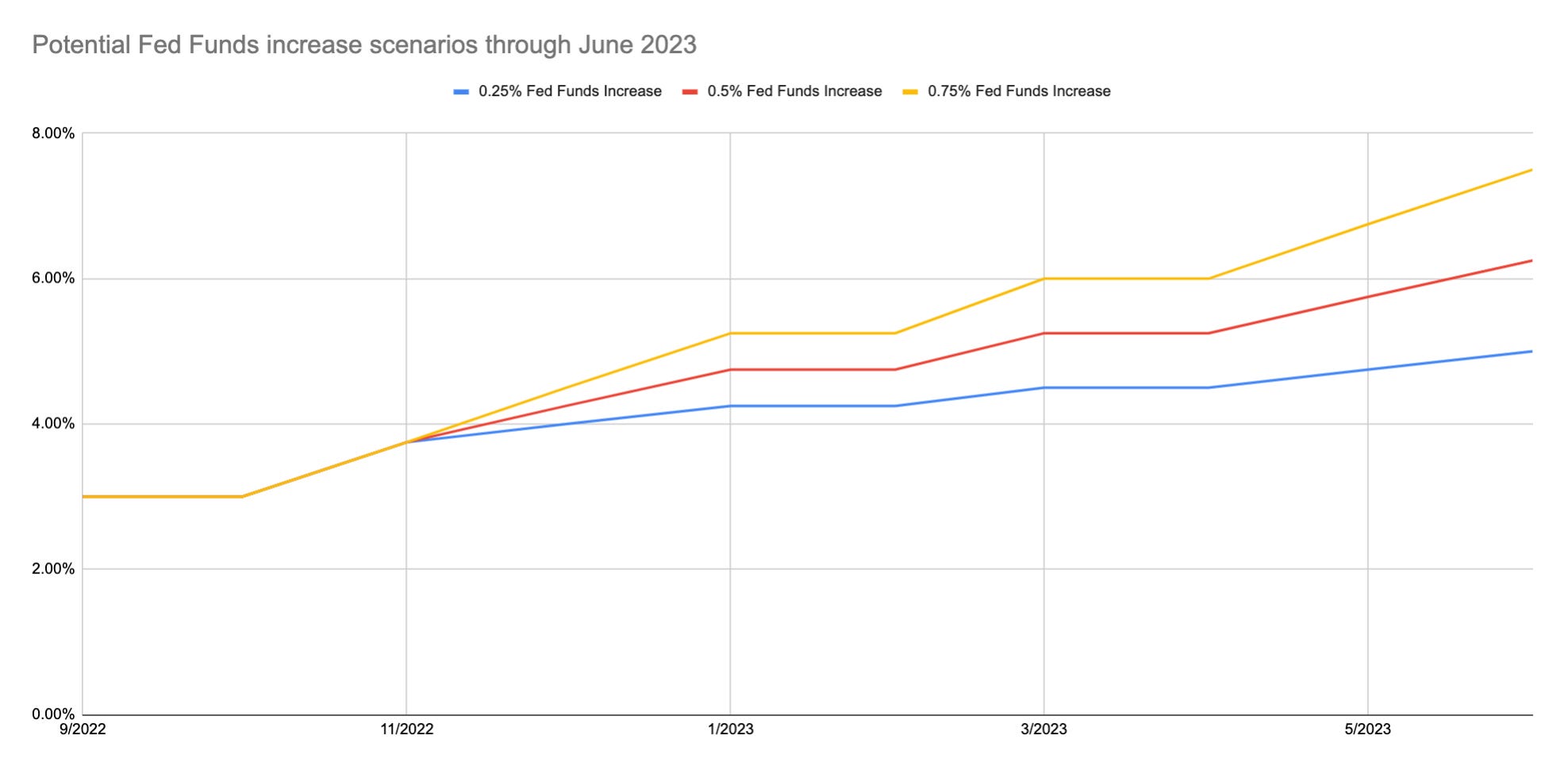

First, we’re going to make a logical assumption that the Fed is going to increase rates by 0.25%, 0.50% or 0.75% at its meetings for the foreseeable future. Playing out scenarios where the Fed sticks to raising by one of those rates consistently, it would look like the below.

The scenarios get us to a range of 4.5% to 6% by April, and 5% to 7.5% by June. So we can see that the Fed couldn’t raise by 0.25% and comfortably stand by its current resolve. A string of 0.5% rate increases lands in a potential sweet spot of 5.25% in April and 6.25% in June if inflation continues to turn, and 0.75% likely overshoots (6% in April and 7.5% in June), but not by much.

What does this all mean?

Takeaways?

None of the exact scenarios that I lay out above are going to take place. However, it shows that any of the rhetoric out there around a Fed pivot / aggressive slow down doesn’t make any sense given its current posture. The most likely scenarios over the coming meetings are either one more 0.75% increase in December followed by a series of 0.5% increases (while they watch CPI), or 0.5% increases starting in December and continuing.

We obviously can’t know for certain, but looking at the math helps. It’s hard to see how the Fed could justify slowing down with inflation’s death as the primary goal. But…let’s sit back, and we’ll know soon enough!

The content of this post, or any post on Stumbling About, is for informational purposes only and does not represent investment advice. You should do your own research before using any of the information that we share, and especially before investing.

The “Fed” is the Federal Reserve, the central bank of the United States

The Federal Funds rate is the interest rate at which depository institutions trade federal funds (balances held at Federal Reserve Banks) with each other overnight; the effective rate is the market-determined weighted average of the rates that banks actually lend to each other out in the wild

Every month, a CPI (Consumer Price Index) report comes out that shows how prices have changed that month relative to the last, as well as compared to the same month last year (this year over year number is what is published as the official inflation rate)

Jerome Powell is the current chair of the Fed

Who knows if this is true, but stick with me!