Don't call it a comeback [Q4 2023 Portfolio Update]

Don't call it a comeback [Q4 2023 Portfolio Update]

The content of this post, or any post on Stumbling About, is for informational purposes only and does not represent investment advice. You should do your own research before using any of the information that we share, and especially before investing.

You ain’t seen nothing yet

That return to all time highs that I mentioned around this time last year is now upon us. And…I don’t think we’re done yet. Happy days are here again!

Well, kinda.

The market continues to show signs of moderately excessive valuations — Nvidia, anyone? — and the economy is still, in my opinion, full of head fake style resilience. But regardless of all this macro mumbo jumbo, it doesn’t look like investors are quite ready to acquiesce. That makes for more fascinating times ahead.

The Fed is talking about cutting rates 2-3 times this year, and the market is hoping for 5-6. Putting politics aside, it doesn’t economically make sense for them to cut right now with inflation remaining not outrageous, but sticky, and interest rates being higher than we’ve been used to for awhile, but in a normal range. Honestly, I think it’s about dag nab time for the Fed to just let the economy play itself out. Avoiding the inevitable is just gonna make the bust even bustier. We shall see.

I’d be surprised if we don’t see another 15-20% pop in the market (at least) in the near term (i.e., this year-ish) given all this enthusiasm. Regardless of how exactly this plays out, it’s gonna be fun!

The usual context setting

My portfolio is primarily based on a Long Trend Momentum model that I created called Farfin. You can learn more about Farfin here. In addition, I will usually also have a relatively small investment in broad market ETFs, concentrated mostly in the Vanguard Total Stock Market Index ETF (VTI)1.

The combination of these typically results in my investments based on Farfin being 90%+ of my portfolio. However, I will opportunistically pick up other stocks when the market calls for it. As of the end of Q4 2023, my portfolio was roughly an 80%/20% split between Farfin and non-Farfin, respectively.

Most of this post will look at the combined portfolio, but I do highlight Farfin performance specifically in the “High level quarter summary” section.

High level quarter summary

Results2: The overall portfolio was up +27.2% for the quarter and +31.1% for the year. Just when you might have counted me out, I came roaring back like a faithful soldier.

Market Results: As a reference point, the market (VTI) was up +12.2% for the quarter and up +26.1% for the year. Cute, Mr. Market….that 2 in front of your returns is simply cute.

Buys: No purchases this here quarter. Just boring old me.

Sells: Nothing bought, nothing sold.

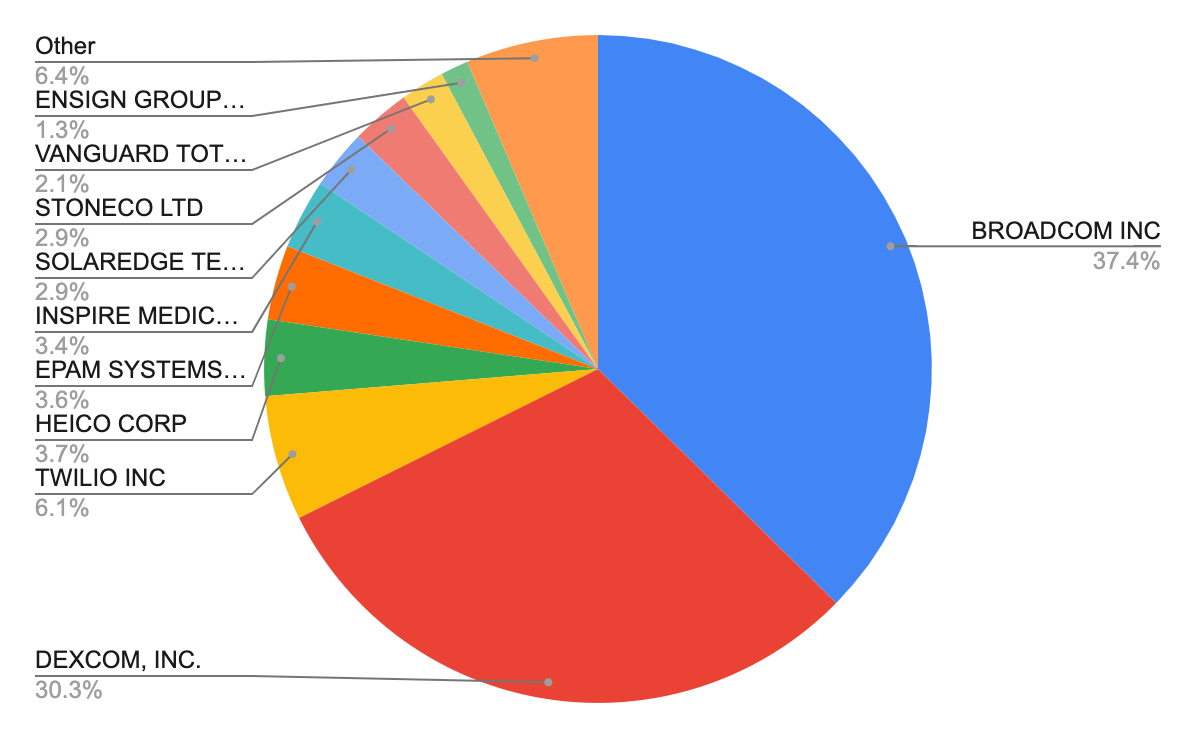

Top Holdings: Broadcom continued to hold onto its dominant lead over DexCom, remaining my #1 holding at roughly 37%, and here’s the full top 5:

Broadcom (AVGO): 37.4%

DexCom (DXCM): 30.3%

Twilio (TWLO): 6.1%

HEICO Corp (HEI): 3.7%

EPAM Systems (EPAM): 3.6%

Top 10 holdings cumulatively: 93.6%

Below is a pie chart of my top 10 holdings for those that enjoy visuals.

Farfin-specific summary

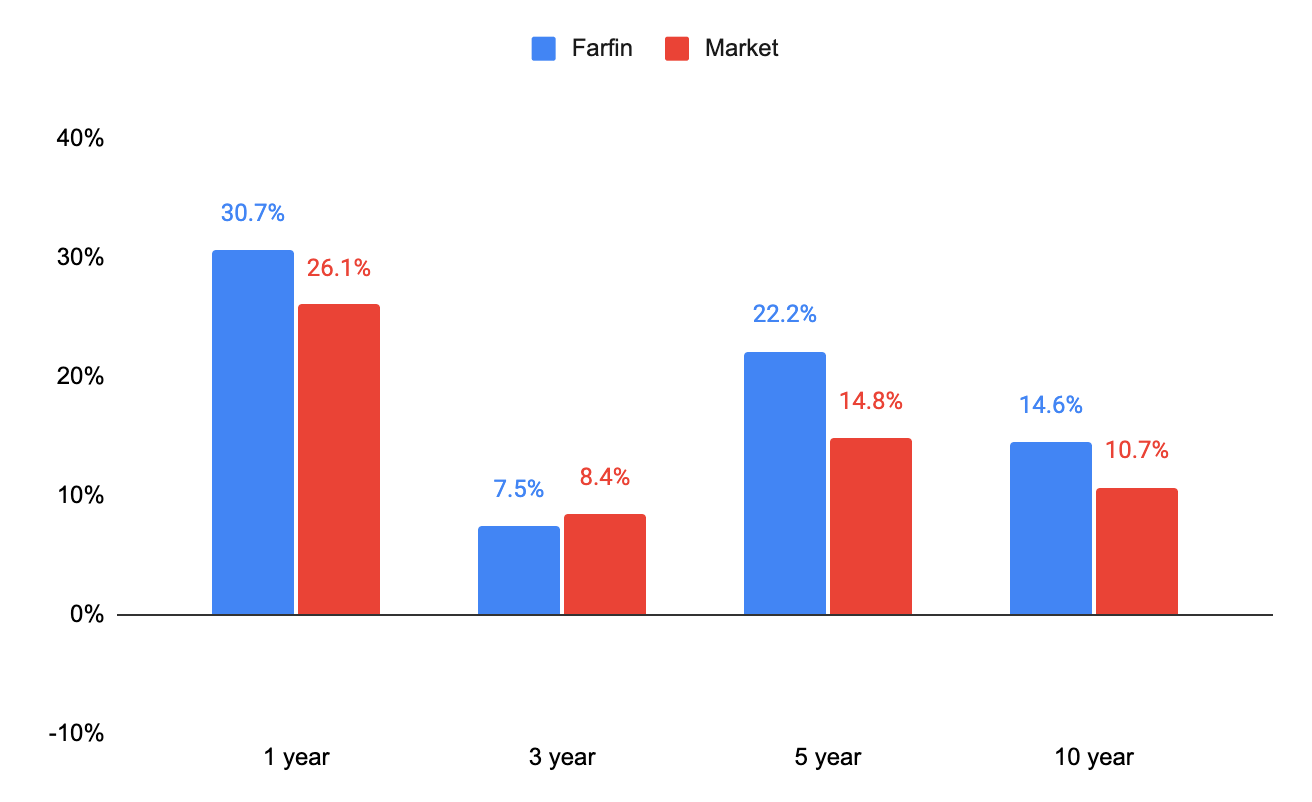

Since it’s the end of the year, I’m going to take a little space to give a summary of Farfin’s performance specifically (reminder that Farfin is the model that dictates the bulk of my portfolio investments).

Below is a quick look at Farfin’s 1 year, 3 year, 5 year and 10 year performance (CAGR) vs. the market.

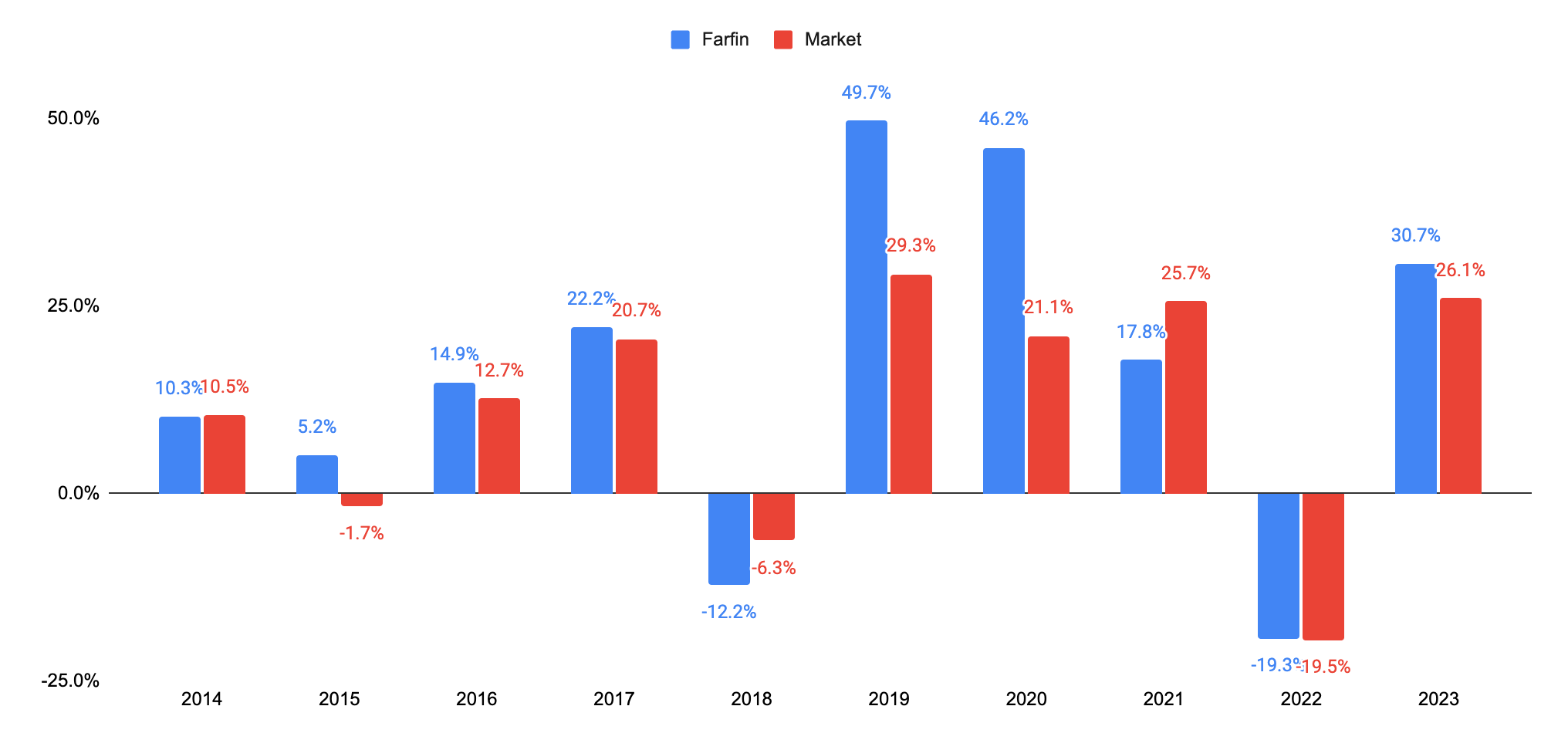

I expect Farfin to outperform the market roughly 60-70% of the time, so this year is helping me out with that expectation. Below is the year-by-year breakdown of Farfin v Market over the last decade.

Lowlights and Highlights

Lowlights

Overall, this was a pretty excellent quarter. However….SolarEdge is the proverbial wet blanket on an otherwise very good time.

SolarEdge (and the solar industry overall) is quite volatile, so I’m expecting a wild ride on this one. It was originally a part of the Farfin portfolio, but I picked it up in my normal portfolio to let it breathe another breath. I’m expecting to hold this one for at least a year to ride that wave back up!

As for the entire year, I’m most disappointed in Inspire Medical Systems. It’s a relatively young public company (~5 years public), and I like picking these young bucks up from time to time in order to be witness to their triumphant ride to glory. However, while that’s how INSP started the year, it fumbled the ball about halfway through and wasn’t able to fully recover.

Here are the 5 bottom feeders for the quarter (full year returns in parentheses):

SolarEdge Technologies (SEDG): -27.7% (-67.0%)

Makita Corp (MKTAY): -11.5% (-14.3%)

Inspire Medical Systems (INSP): +2.5% (-19.2%)

Carrier Global Corp (CARR): +4.5% (+39.8%)

NextEra Energy (NEE): +6.9% (-25.3%)

Highlights

This my friends, was a good quarter 😊

Quality performance was rampant, but I’m going to focus on three — StoneCo, DexCom, and Broadcom.

StoneCo is a Brazilian financial technology and services company and it was been beaten down aggressively from Q1 2021 to Q1 2022 (as you can see in the chart below). Since then it’s sat in a range between ~$10 to ~$18 per share. I see a lot of promise in the company (and the stock!), and love that they’ve done great work in getting to profitability. There’s lot of money to be made down in Latin America!

I’ve bought Stone in several tranches, starting in Q4 2021, with my average purchase price at ~$13 per share. I feel pretty good about the stock’s near-and-medium-term prospects. In Q4 2023 Stone shot up nearly +70%, giving it a full year return of +91%. Loving it 😊

I’ve written about DexCom plenty on here, and was so so happy to see my turnaround thesis for the stock take shape so quickly. You might recall that DexCom got stomped on in Q3 with the continue uptake and threat from the weight loss drug craze. I didn’t see reason to believe that these drop would have real negative impact on DexCom’s business, so I bought more! And, so far at least, DexCom has not disappointed, providing a +33% return in Q4.

Now, let’s save the best for last. Broadcom, Broadcom, Broadcom. Wow!

Broadcom continues to be a fantastic company and stock. It provides solid top line growth, profitability and pays a healthy dividend of ~1.5%. Two things were most material for Broadcom’s business last year: 1) the acquisition of VMWare, which closed in November; and 2) AI.

While Broadcom didn’t get all the AI boost that made Nvidia and Super Micro powerhouse stocks last year, I am not complaining. In Q4 Broadcom brought in a +35% return, and it more than doubled over the course of the year. It now has an even firmer grasp on the top spot within my portfolio.

Here’s the full top 5 quarterly best performer list (full year returns in parentheses):

StoneCo (STNE): +69.0% (+91.0%)

Broadcom (AVGO): +35.0% (+104.2%)

Dexcom (DXCM): +33.0% (+9.6%)

Twilio (TWLO): +29.6% (+55.0%)

Dollar General (DG): +29.2% (-44.1%)

Looking to the future

Overall: The market continues to be bullishly strange, and I expect the good times to continue as least for a little bit. Jay Powell and the election are obviously going to be the most important factors (that we know of right now) for this year’s performance.

To sell: I’m keeping an eye on Philips, Makita and Dollar General as potential sells. This will also be a critical year for Twilio and whether my general thesis on the company’s prospects show more signs of coming into fruition.

To buy: Beyond the Farfin-based buys that I made at the start of the year (which you’ll see in next quarter’s update), I’m watching Alibaba (BABA) and Daqo (DQ). If these stocks were anywhere besides China I would’ve already pulled the trigger, but that place has shown me how unpredictable is can be so I’m treading lightly.

Oh, and if interested, you can see my whole end of Q4 portfolio here — these are all my holdings, along with performance for the quarter. Enjoy!

The content of this post, or any post on Stumbling About, is for informational purposes only and does not represent investment advice. You should do your own research before using any of the information that we share, and especially before investing.

Throughout this and other posts, when I refer to a stock’s performance relative to “the market”, I’m using the Vanguard Total Stock Market Index ETF (VTI) as the proxy for “the market.”

All of my returns are calculated using time-weighted returns.