Deal or No Deal?

Deal or No Deal?

aka, this market is bonkers and I'm loving it

The content of this post, or any post in Stumbling About, is for informational purposes only and does not represent investment advice. My investing style is fairly aggressive, and suits my own personality and psychology…it may not suit yours. You should do your own research before using any of the information that I share, and especially before investing.

What a market…

Let’s begin with a few facts if you please. 2022 has had:

The worst first 4 month start to a year for equities since 1939 (yes, the same 1939 that occurred during the Great Depression)

The worst start to a year for the bond market since 1842 (yes, the same 1842 that marks the founding of Notre Dame University)

Intraday swings usually reserved for monster crash or recovery years feel quite commonplace

A Nasdaq that’s in a bear market and an S&P that is double dutch style looking like it wants to be a bear too

So what is an investor to do in such a market? The sensible answer is nothing - don’t look at your portfolio, and just sit and wait this thing out. However, for the next few minutes I ask you to put your sensibilities aside and let’s have some fun.

How bad is it really?

I’ve read about how many stocks are getting hammered right now, but looking at the detail is quite another story.

Over 80% of individual stocks trading in the US are at a -20%+ drawdown, over 65% are at a -30%+ drawdown, 45% are at a -50%+ drawdown, over 25% have drawdowns of 75%+, and more than 5% are down 90% or more. Ouch!

And this isn’t just a US company thing either. Here’s a quick look at median drawdowns by country for the worst performers (50%+ drawdowns)1:

China. Wrecked.

Canada. Wrecked.

Israel. Wrecked.

Even the United Kingdom, which has been held up as a beacon of cheapness for the last couple years has a median drawdown of -39% (it was below the cutoff at #28).

So at the market level it’s not good, but not terrible. But at the individual stock level there’s some real horror.

But this time is different

The saying “this time is different” usually gets me in a tizzy. I’m a strong believer in history rhyming (not repeating), and don’t like it when people use “this time is different” to justify their own actions.

That said, economically, we’re in some unprecedented waters, so it’s worth stepping back and taking a look at why it might be different and why it likely just isn’t.

Why it might be different

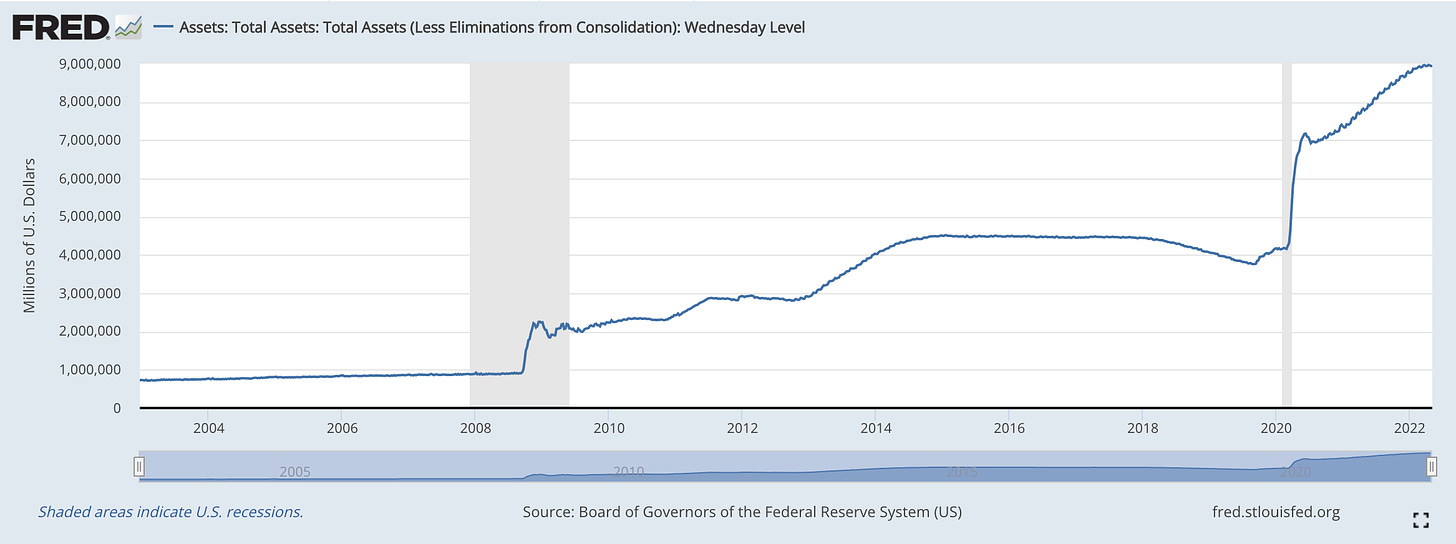

We’ve had the Federal Reserve feeding unprecedented amounts of money (a net increase in assets of $8 million million2) into the system for over a decade…and now they’re stopping (below is a chart of the Fed’s balance sheet since 2002)

Assets of all classes started the year at or near all time highs (bonds, stocks, gold, crypto) — take a look at my Bullishly Pessimistic post linked below if you want to see charts

Inflation is at 40 year highs (speaking of which, if you haven’t looked into Series I bonds, please go do so now…9.62% relatively risk free is nothing to scoff at)

The Federal Reserve is having large interest rate increases (0.5%+) for the first time in over 20 years, with more potentially coming

Russia has been on the verge of potentially starting World War III

Other reasons to be pessimistic (but bullishly so)

Why it just isn’t

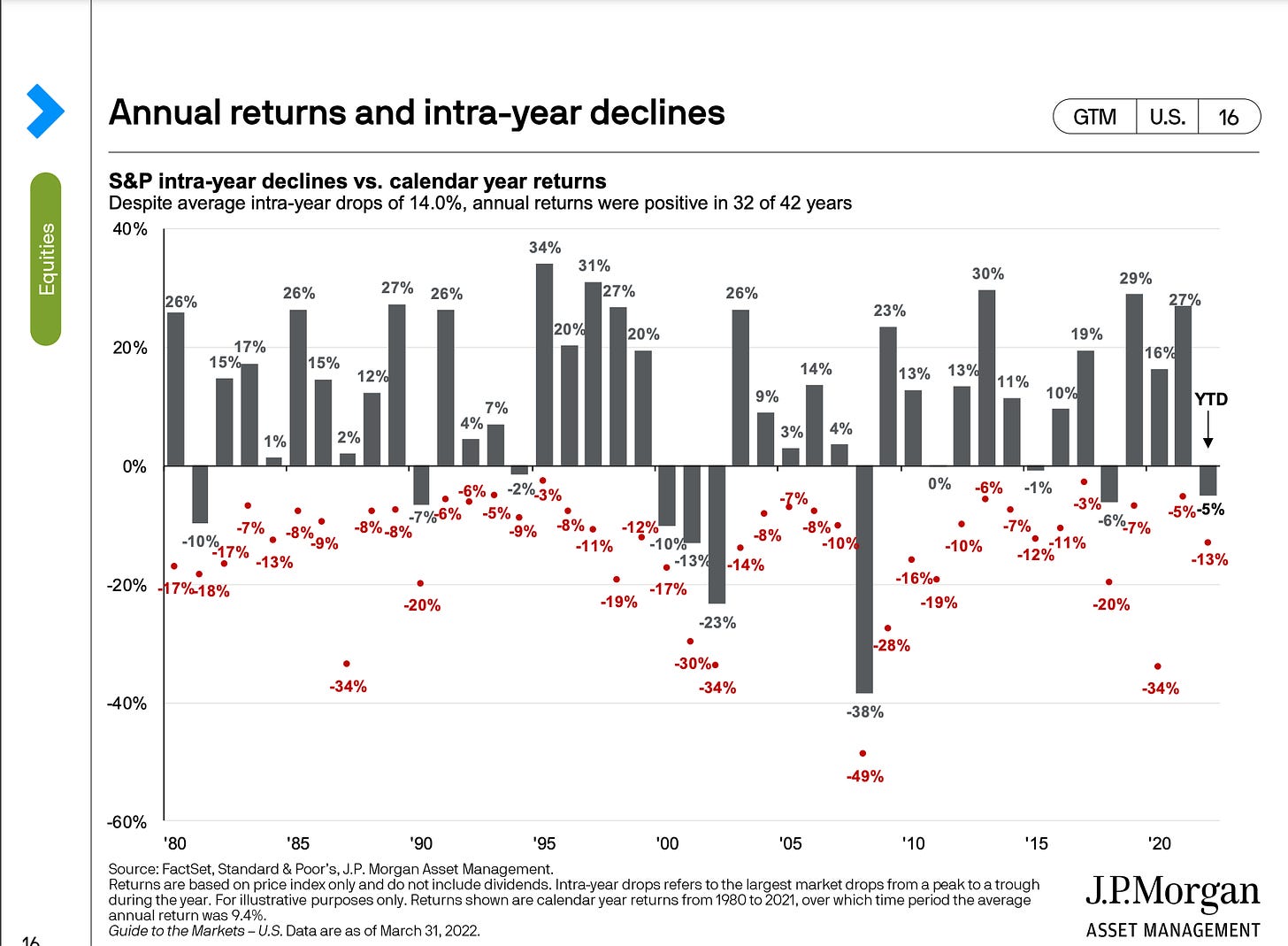

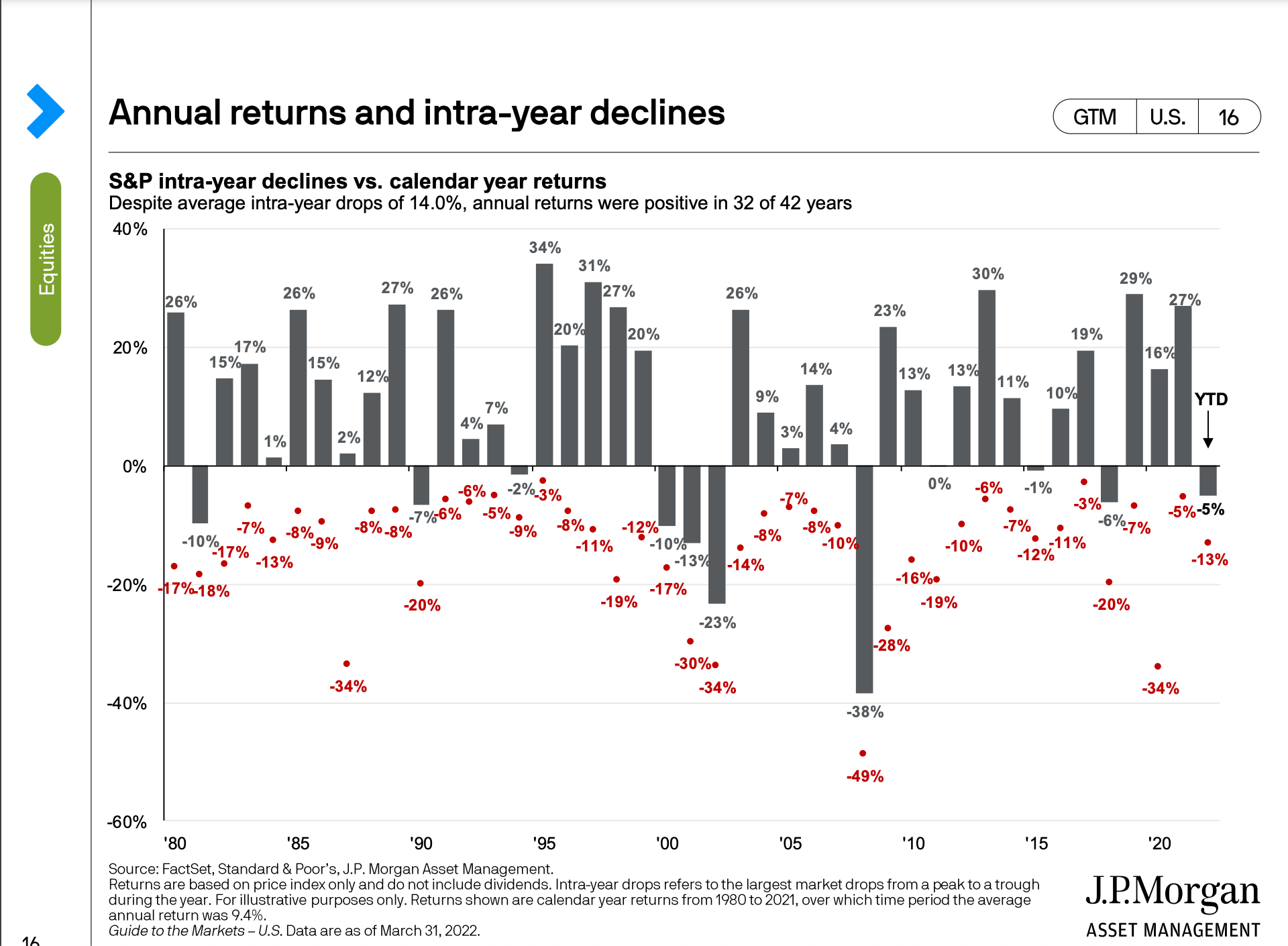

Drawdowns3 happen all the time — on average the stock market has an intra-year drawdown of -14%

Interest rate increases — it’s true that in the US, we don’t often have 0.5%+ increases to the Federal Funds rate. And it’s also true that we’ve been in a 40 year downward trend in interest rates. However, it can’t be too surprising that the Fed is raising rates. We do this every few years, and yet every time the market acts as if it has been violated

Mean reversion — value investors preach this gospel infinitum. Mean reversion is just a thing that markets do. If it goes down lower than it should, it comes back up. If it goes up higher than it should, it comes back down4.

Companies are for the most part beating their estimate revenue and earnings targets — with over half of S&P 500 stocks reports, over 80% have beaten estimates. That’s a little over the average of 77% over the last 5 years5.

So when folks are saying that this is “the opportunity of lifetime” or that it’s different, most of that is coming from having a limited perspective. Famed investor Bill Gurley nailed this in a tweet a couple weeks back:

So…now what?

I don’t have a crystal ball. This could be the start of the next big crash6. This could be the start of a new covid crash style rally. Who knows.

But, just for fun, imagine that we 1) believe that the market is the near bottom, and 2) have a Buffet-sized boat load of cash to deploy. As such, we decide to go shopping. Where would we look?

My investing approach doesn’t live in the world of indices, so put those aside and let’s just examine individual companies’ stocks. Specifically, right now I like stocks that:

Trade on a US exchange (~5,600 stocks)

Are having material drawdowns (-50%+)

Are good companies and good stocks, which can be either of the below or both:

It performed well in a non-spiky way before the recent drawdown (beat the S&P 500 by at least ~50% over the last 5 years relatively smoothly)

It has solid financial fundamentals and/or dominant, moat-like market positioning (this one is much more art than science)

What’s catching my fancy

Reminder, this is by no means investment advice. The following are stocks that have caught my attention based on my own risk tolerance, investing style and can do attitude.

I’m going to skip the nitty gritty details of prices, cash flows, earnings, 10ks, etc and skip to the punch line7.

Of all the ~5,600 stocks trading in the US, I found 9 (~0.2%) that I’m keeping a close eye on8. For the most part these would fall into the category of “growth stocks”, but there are some boring companies in here too. Let’s start with those.

The Boring

Boring is not bad — sometimes a little boring is just what the doctor ordered.

Makita Corporation (MKTAY): Makita is based in Japan, founded in 1915, and sells power tools. Solid growth and I like the fundamentals. I think Makita is worth a little research under a $30/share price tag.

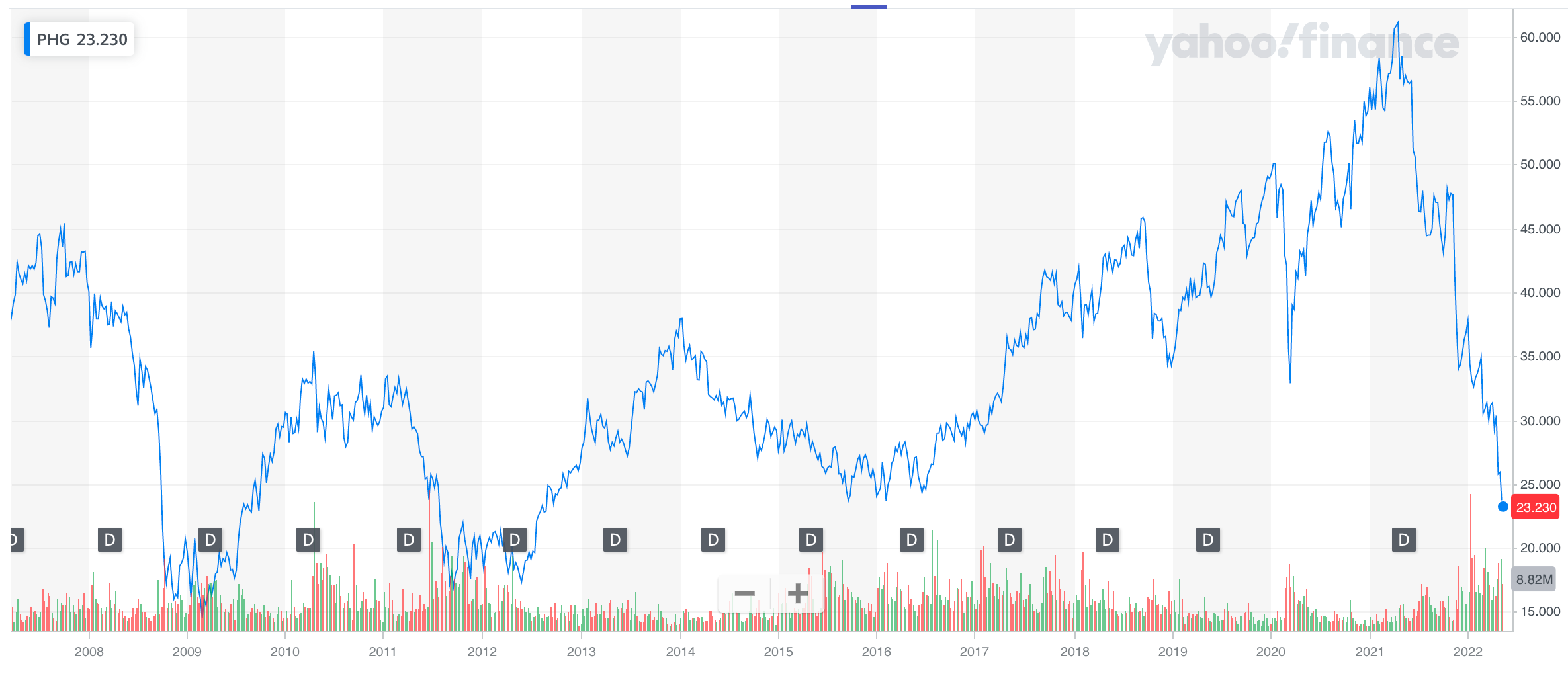

Philips NV (PHG): If you’ve ever used a light bulb, been to a hospital, or shaved…chances are you’ve used a Philips product. Based in the Netherlands, Philips has historically been Europe’s equivalent to General Electric (they were founded one year apart in the late 19th century, and both created huge diversified conglomerates over the next century). There are many things to like, including the dividend. Worth a look under $27/share.

Aflac (AFL): Aflac is the odd stock out within this list because it hasn’t been hit nearly as hard as the others. However, I couldn’t help but include it. This is a solid company, good growth, good dividend…and is a backdoor bet on Japan9. As I mentioned, Aflac isn’t flying low at the moment, but if you see it creep down into the $40s, I recommend doing your homework.

The Growth Bets

Alright, now for the “fun stuff.” These are the stocks that could be high fliers or falling machetes. Either way, I like what they have to offer.

Alibaba (BABA): This company has been all over the news, so likely already on your radar. The big question here is whether or not China will let the company grow untethered. The historical growth is big, the fundamentals are good and this could be a wild ride should China let it run. Under $100 it’s worth the research, and under $75 it’s just silly.

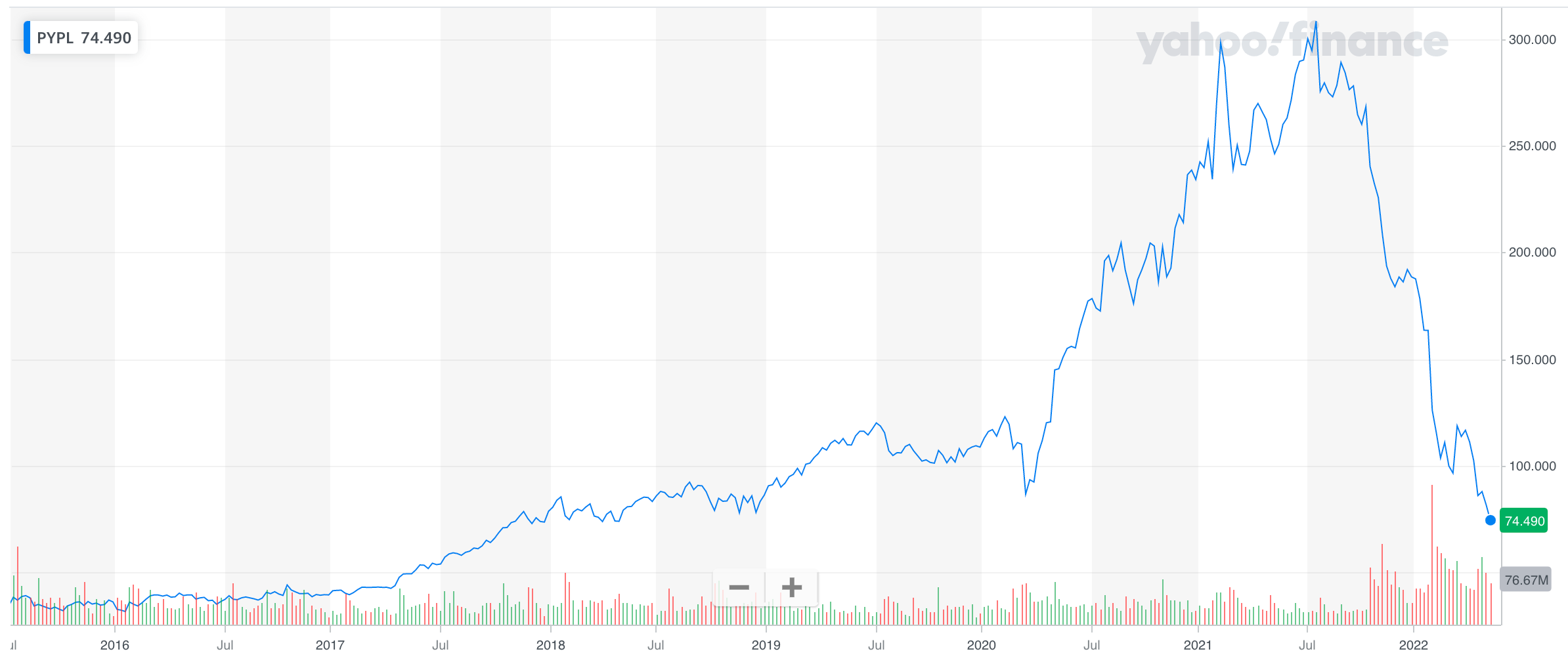

PayPal (PYPL): You know what PayPal does (i.e., payments to pals), so I’ll skip that. This company, and this stock, have outplayed the competition over the years through thick and thin. I like their leadership and their market positioning. Under $85, it’s worth reading through their financials and 10k, and if it falls into the $50s I’m really going to get excited.

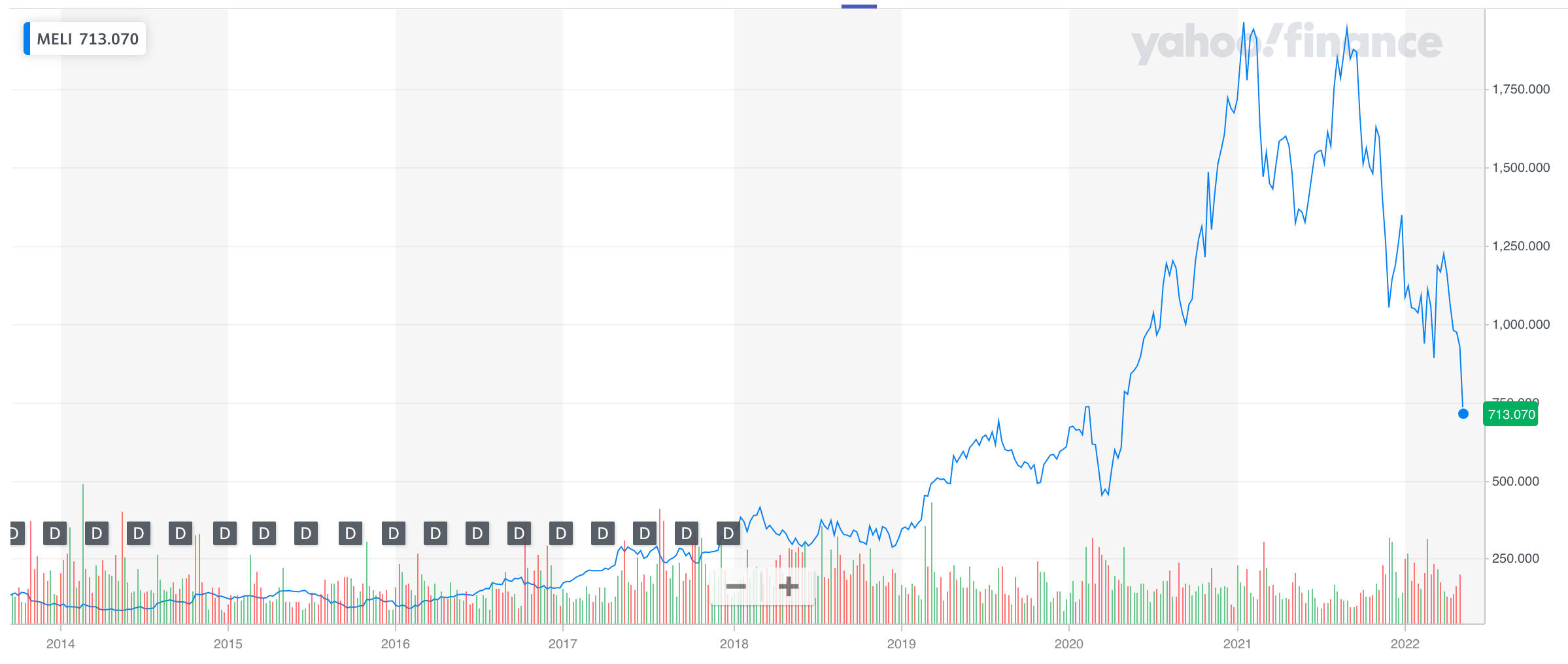

Mercadolibre (MELI): Mercadolibre is often described as the “Amazon of Latin America”. It’s based in Argentina and has growth coming out the waheezy. This one has a little further to go before I think it gets interesting, but worth keeping an eye out. If it crosses $650, that’s interesting, and if it crosses $600 that’s fascinating.

Twilio (TWLO): I love me some Twilio. Twilio is the communications technology behind many products that you use all the time — e.g., if you hail an Uber, Twilio is what controls the comms. They’ve more recently ventured into other markets like contact centers and I’m stoked for the potential for growth and absolute market dominance. As far as the stock, it’s been pricey, but is now coming back down to Earth (at least moreso). Under $100, it’s worth a look and under $70 is when the shoulder shimmies start.

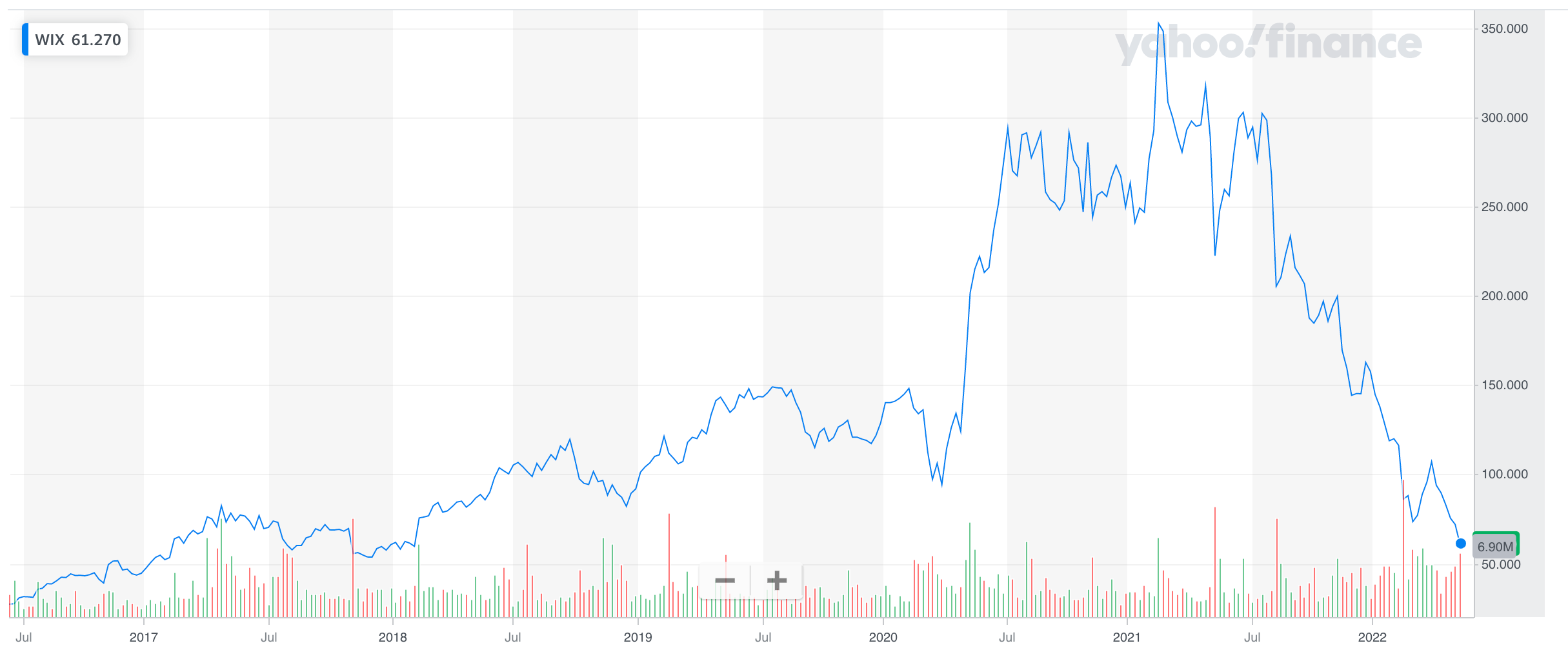

Wix.Com (WIX): Wix is based in Israel and was an early player in the more recent no-code / create your own website space (kind of like Squarespace). Good growth and good prospects. As the no-code market continues to gain steam, it’s worth keeping an eye on, especially under $60.

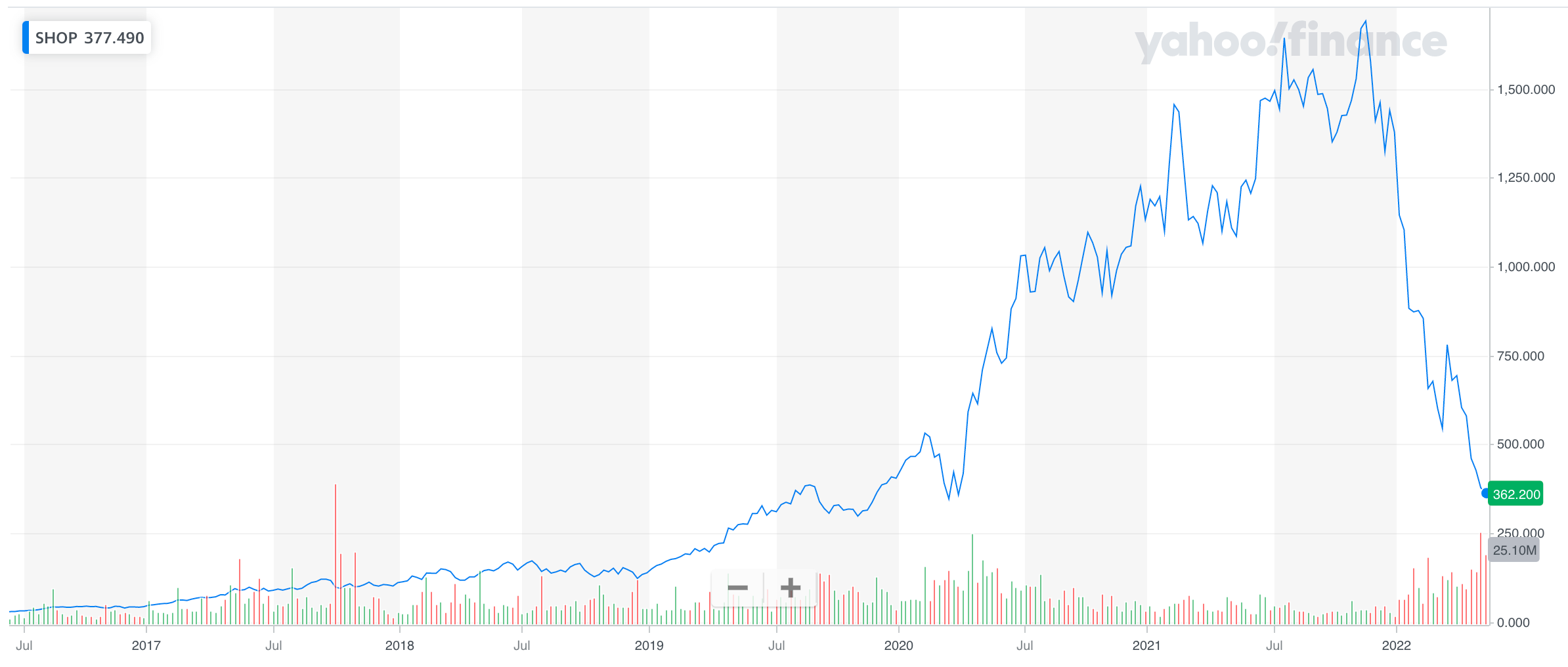

Shopify (SHOP): Wrapping up the finds is Shopify, Canada’s answer to Amazon’s decades-long ecommerce dominance. This company has a great founding story, distinguishes itself through merchant-centricity, and has proven that they’re able to compete. The question is whether they can fully cross the chasm to wrestle with the big cap companies, and only time will tell. I like this company and this stock. Worth a look under $350 and a triple take under $250.

What a market

Going to close this out how it began. What a market and what a time to be an investor. The days are painful, but over the long term it can be a fun ride.

Stay invested, stay learning, and thanks for reading.

The content of this post, or any post in Stumbling About, is for informational purposes only and does not represent investment advice. My investing style is fairly aggressive, and suits my own personality and psychology…it may not suit yours. You should do your own research before using any of the information that I share, and especially before investing.

Reminder, that these don’t include all of the stocks from companies in each country, but rather they are the stocks of those companies that happen to trade on US exchanges (which can be a small fraction of most countries’ publicly listed stocks)

Yes, technically $8 million million is $8 trillion, but $8 million million just sounds bigger

A drawdown is the percentage drop from the last high price to the last low price in the market

Note that I used the phrase “than it should.” I’m not saying that everything that goes up comes back down, nor that everything that goes down comes back up. But when those price swings get buck wild out of proportion to the inherent value of an assets, reversion tends to happen.

If you’re interested, here’s a look at earnings and revenue surprises over the past decade or so.

I don’t think it is, though I do believe the crash is coming soon (definition of soon TBD)

I’m sorry if you were in this for the detail…

Close eye does not mean buying necessarily 😄

Aflac is based in the US but gets the majority of its revenue from the Japanese market