Bullishly Pessimistic

Bullishly Pessimistic

The content of this post, or any post in Stumbling About, is for informational purposes only and does not represent investment advice. My investing style is fairly aggressive, and suits my own personality and psychology…it may not suit yours. You should do your own research before using any of the information that I share, and especially before investing.

For over 2 years, I’ve been talking about the cataclysmic end to this stock market party. Since then, the market is up over 40%, and my personal portfolio is up nearly 70%. So……was I/am I wrong? Not exactly.

I do still believe that we are approaching a rather massive, multi-year market crash. And I’m also still pretty heavily invested in the market — hence being bullishly pessimistic. This post lays out why this is the case.

The Pessimism

During a recent stock market rant to my brother-in-law, he asked me why, specifically, I think the market is gonna tank. I laid it out for him, and since I hadn’t put all of the puzzle pieces together down in writing before, I figured why the heck not.

First, it’s important to note that I don’t believe that any one thing ever causes a crash. The stuff that leads to market crashes are standard fare that happen all the time. It’s when this standard stuff happens at a time when the market is at a place of intolerable fragility that things go awry. Below are my not-so-comprehensive lists of what’s leading to market fragility, and what could be the triggers that lean on that fragility.

Increasing Fragility

The US stock market has proven to be quite a resilient system. Over the last ~100 years, it has taken on multiple wars, depressions, recessions, etc. and still booted out the chart below (this is the S&P 500):

That represents a ~10% annual return from the mid 1920s until the end of 2021 — pretty solid. As Warren Buffet often says, it hasn’t been smart to bet against the American stock market.

However, every now and again (about every 10 years or so actually), fragility builds in the system, and betting on the market gets scarier and scarier. We’re approaching one of those times, with the four predominant fragility causes being:

Debt: every part of the economy is at a record level of debt

Valuations: nearly every major asset class is near a record level of valuation

Consumer sentiment: people aren’t particularly optimistic

Employment: people aren’t working, and aren’t looking for work either

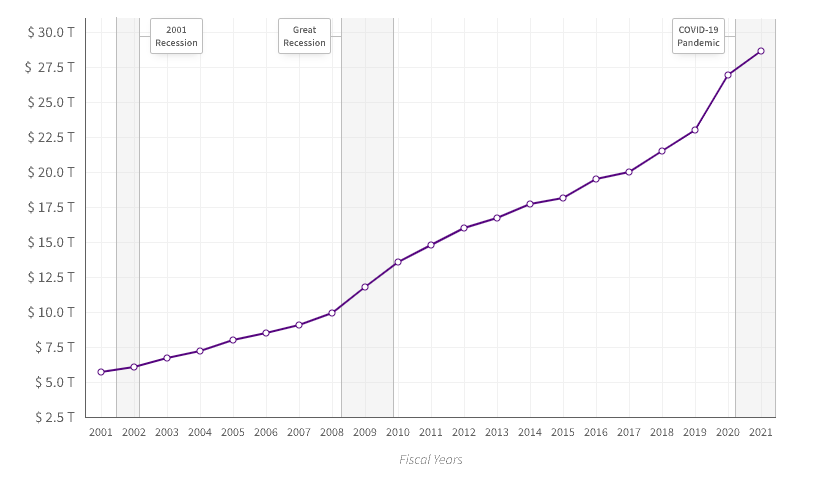

Record Levels of Debt

I’ll just let the numbers speak for themselves. First up, government debt.

Source: USA Spending

Next up, consumer debt.

Source: New York Fed

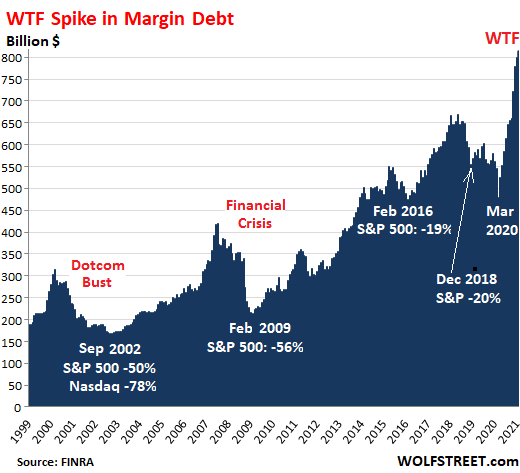

Next, investment debt (i.e., margin debt).

Source: Wolf Street

And last, corporate debt (this chart includes only non-financial companies, but you get the idea).

Source: St Louis Fed

Record valuations

US stocks are way up (remember this graph from before?).

US bonds are way up. Here is the 10 year treasury yield over the last ~60 years (and remember that yields move in the opposite direction of prices).

Source: Macrotrends

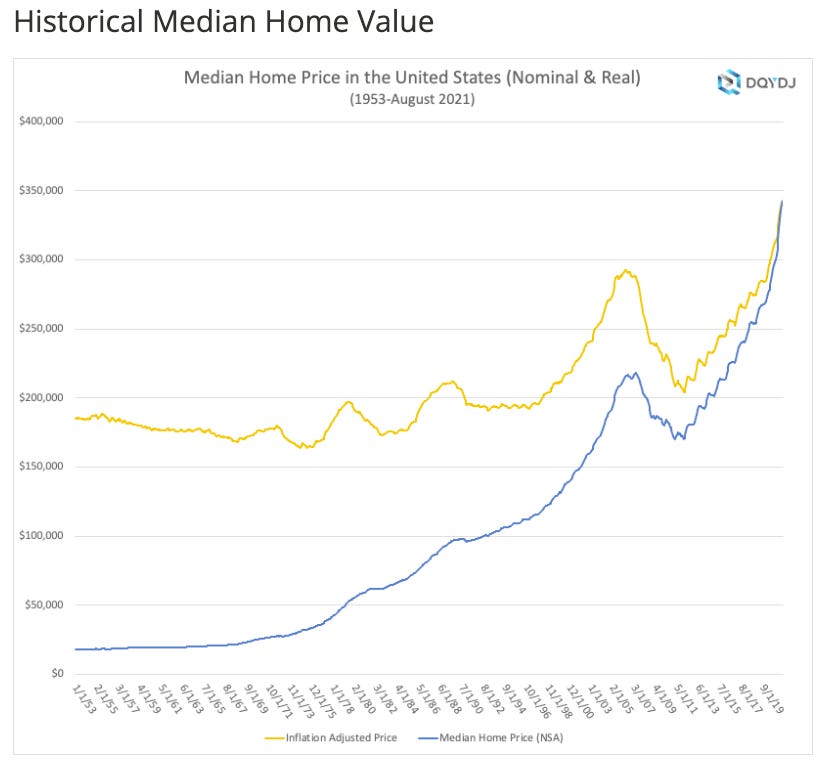

Housing…

Source: DQYDJ

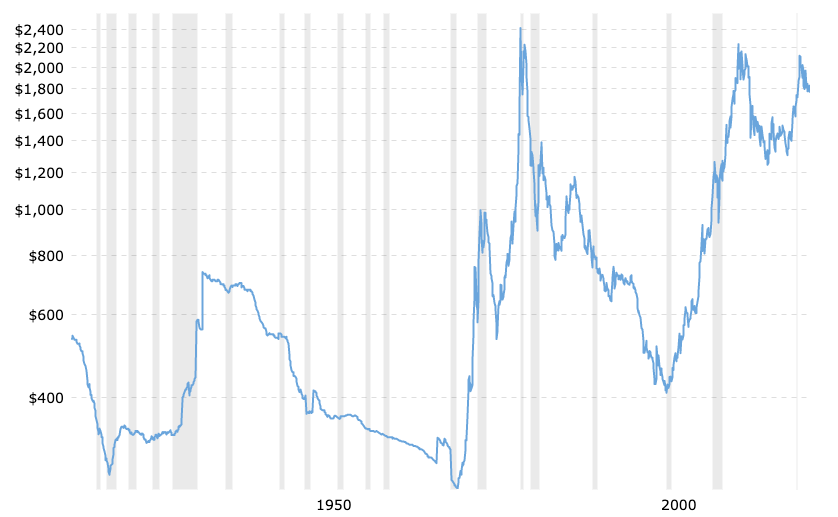

Gold, because why not.

Source: Macrotrends

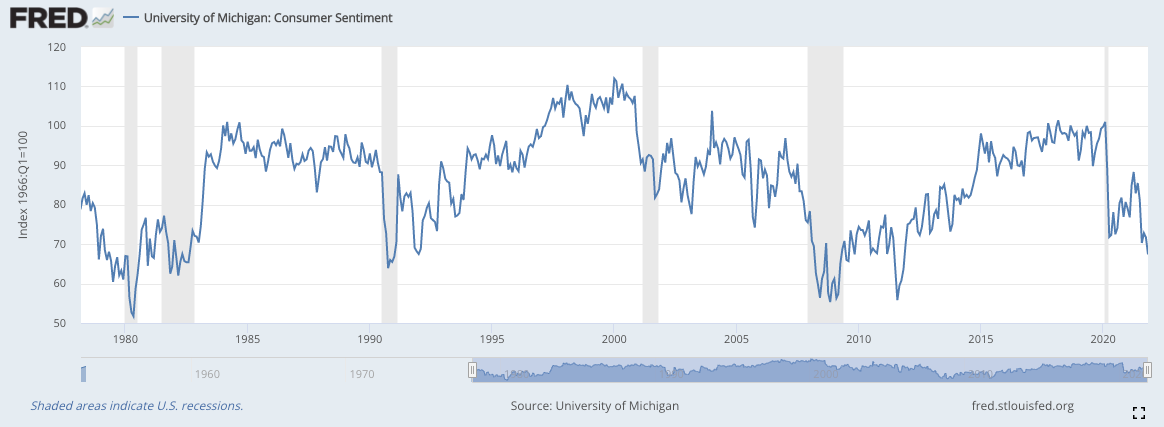

People Aren’t Particularly Happy

The stock market is fueled by emotion — specifically, our feelings toward the future.

Source: St Louis Fed

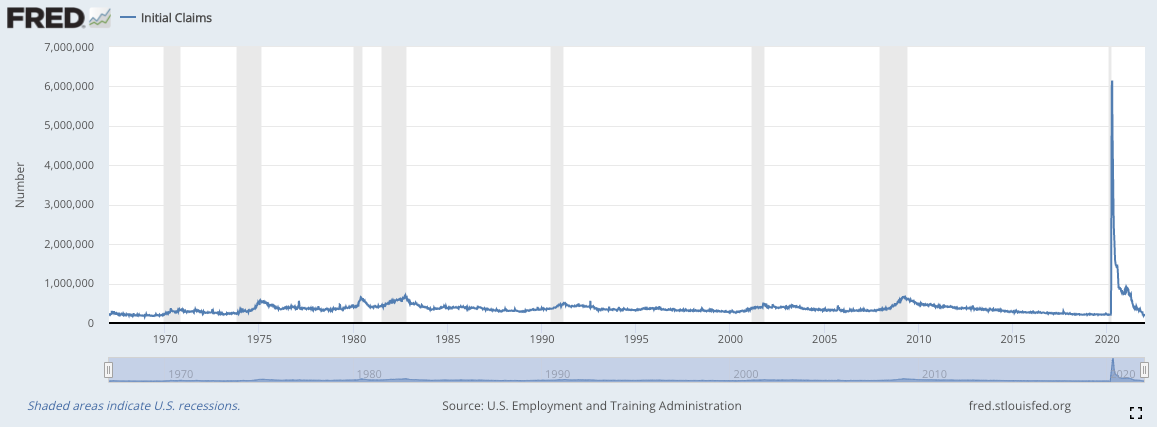

People Aren’t Working

This one holds true importance to me because working leads to wages; wages lead to cash in people’s pockets; cash in people’s pockets leads to the ability for people to manage through shocks. With people working less and less, and also not looking for work, it makes me pessimistic about the ability for consumers to handle any financial negativity…

Source: St Louis Fed

Unemployment is low, and…

Source: St Louis Fed

…people aren’t claiming unemployment. Issues here are delayed for now, but I suspect that there will be a reckoning once more folks need access to cash.

Alright, now that I’ve shown why I think things are fragile, what might be the metaphorically camel back-breaking straw?

Triggers

In short, I don’t know what's going to start the spiral, but here are my current running hypotheses:

Inflation + interest rates

Corporate bankruptcies

Declining corporate earnings

I don’t view the above triggers as mutually exclusive.

First, it seems likely that the Fed will need to aggressively increase interest rates to fight inflation (remember, inflation is showing itself to not be “transitory'“ as Powell once said). They’ve already said they’re going to raise in 2022, but I think it might be more aggressive than we think.

If the Fed aggressively raises interest rates, then that debt that we talked about before might become quite a problem. This is true for consumers, especially if they aren’t working, and aren’t trying to work. And this is true for companies, especially so-called zombie companies — companies that can’t support their operations through the normal course of business, and therefore rely upon borrowing (i.e., going into more debt) in order to stay alive. If their debt payments increase, and access to funding decrease, that’s no bueno.

And this takes me to the corporate bankruptcies mentioned above. Zombie companies going bankrupt will be one thing, but it’s the unexpected corporate bankruptcy that will really be the problem. I don’t know what company (or companies) this will be, but given the level of corporate debt it would be surprising if the change in a business cycle doesn’t put unforeseen pressure on some large indebted company to the point where they must call it quits.

Independent of bankruptcies, downward pressure on consumers’ ability to spend (given all of the above), and increased debt servicing obligations, will likely have a negative impact on corporate earnings. And, ultimately, when you get past all the emotion, corporate earnings prop up markets. Currently, corporate earnings are at all time highs, and that is noted by many as to why we should expect the current bull market to continue….but I see a major threat to the current earnings trend to be able to continue past 2023 (if not 2022).

So Then, Why Bullish?

OK, so now that I’ve made everyone (including myself) fearful and tearful, why am I bullish?

Well, there are 2 main reasons:

I have a very long term (i.e., multi-decade) investment time horizon. Pullbacks are inevitable, and the US has seen its fair share, but I believe in the US stock market over the long term.

To manage my own psychology, I created my own personal indicator to give me an objective (well, mostly objective) tool to use to shape my annual investment strategies. And the indicator says it’s not time yet, but we’re close — you can read more about my indicator here.

Some might take the pessimistic view above and clear out their portfolio, put cash under the mattress, or similar. But it’s important to remember that portfolio returns are often driven by being in the market on a small number of unpredictable days — if you miss them, then you miss the primary driver of investment returns…compounding.

That said, it is critical in times like this to recognize where we might be in the market cycle, and not to take undue risk. For example, if you put your portfolio into debt that you can’t afford in order to take risks that you believe are certain (these are the YOLO portfolios filled with meme stocks, crypto, NFTs, etc. ), then you are more likely to both lose your money now AND lose your money when the market gets hit. Once again, you’ll miss out on compounding.

I feel good about being pessimistic. It keeps me on my toes, keeps me aware, and keeps me informed. But I feel even better about being bullishly pessimistic — staying involved and staying invested is the path to compounding. And compounding is the whole point of investing.

The content of this post, or any post in Stumbling About, is for informational purposes only and does not represent investment advice. My investing style is fairly aggressive, and suits my own personality and psychology…it may not suit yours. You should do your own research before using any of the information that I share, and especially before investing.